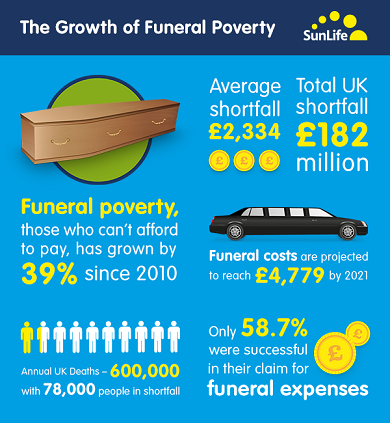

New research reveals funerals costs have more than doubled in a decade. Insurers Sunlife found the cost of a funeral has soared by 5.5% in a single year, averaging £3,897.

One in seven people who have organised a funeral in the past four years admitted it caused them serious financial concern, with the average funeral shortfall standing at £2,334.

However the Fair Funerals campaign urge people to consider their options carefully if they’re thinking about buying a funeral plan.

David Armitage, whose wife died unexpectedly, says:

When Carol died I was in shock. I wasn’t in any state to be looking around different funeral directors for the best price. Carol was in the hospital for weeks after she died whilst I tried to figure out how I was going to raise the money for her funeral. I didn’t feel comfortable with this at all, but what could I do? I didn’t get any support from the government because although I’m a pensioner, I’m on the wrong kind of benefit. The funeral director quoted us £5,000 at first but when we told him we couldn’t afford this, the bill came down to £2,500. In the end my step-daughter paid for the funeral on her credit card, but this left her with a huge debt and high interest to pay. I really worry about how many other people find themselves in this situation after they lose someone.

Heather Kennedy, the Fair Funerals Campaigns Manager says:

Funeral costs have been rising way above inflation for over 35 years. This situation can’t continue. This means a dignified funeral is out of reach for millions of people. Everyday crippling funeral costs are causing grieving families distress, trauma and unmanageable debts.Our MPs need to follow the Scottish Government and develop a plan for tackling rising funeral costs. Despite a damning report from the Work and Pensions Select Committee earlier this year and repeated calls from the concerned public, the government have still failed to take any meaningful action to address funeral poverty.

Funerals costs are rising so dramatically partly because there is no price competition in the funeral industry. Put simply, when we’re grieving we don’t shop around. If we did, we’d realise there’s huge differences in what funeral directors charge.

Given the vulnerability of their customers, funeral directors should be actively trying to help them find a funeral within their budget, which includes putting prices on their website. This is what our Fair Funerals pledge asks them to do. We applaud the third of the UK funeral industry who have signed up to the pledge, but this still leaves the majority of funeral directors without any prices on their website.

Last week the Guardian reported stark differences between the prices charged by different funeral directors for the same goods and services. They found the second largest UK funeral chain Dignity was easily the most expensive costing around £1,000-£1,500 more than independent firms.

Some advice if you're considering a funeral plan

If you’re thinking about buying a funeral plan, you need to shop around and consider your options carefully. Funeral plans are not always transparent about what they provide and what terms they include, and people can end up getting a nasty shock.

- Many funeral plans don’t cover the full cost of a funeral. You should check whether the plan guarantees to cover all the costs or only provides a lump sum. You might be able to save money elsewhere and end up with a better lump sum.

- If the plan says it covers the full funeral bill, you should check what contribution it makes to third party costs. These are the costs the funeral company pays to other providers on your behalf, most significantly to the provider of the burial or cremation. These costs can be up to half the overall funeral bill. Many funeral plans don’t cover full third party costs, or won’t keep up as these costs rapidly increase over time.

- Other plans restrict you to a specific funeral provider, which may not represent the best value of money for you. And it could also be awkward if you move house or if the funeral company closes down.

- Lastly, you should check what happens if a payment is missed. If you change bank account, overdraw or simply forget: will they alert you? Will they accept a late payment? Or will a missed payment cancel the policy?